Table of Contents

I. Rising Equity Activism in Japan: Structural Pressure Builds

In recent years, Japan’s corporate governance landscape has shifted dramatically. Once known for passive investor engagement and entrenched management hierarchies, Japanese public markets are experiencing a tangible increase in shareholder activism. Driven by persistent valuation discounts, weak returns on equity, and growing pressure from both domestic institutional investors and global funds, activist campaigns are becoming more frequent and impactful. According to Reuters, a record 52 Japanese firms received activist shareholder proposals in the June 2025 AGM season, more than four times the number in 2018–2019, with many companies pre-emptively engaging with activists to avoid public confrontations.

Further underscoring this trend data from Barclays showed a record 56 activist campaigns targeting Japanese firms in 2025, making Japan one of the most active markets globally outside the U.S. for equity agitators.

The substance of these engagements has broadened beyond traditional governance demands to questions of capital allocation, strategic focus, board composition, and shareholder returns. Several high-profile campaigns have forced meaningful changes in board makeup and dividend policies across sectors. In parallel, Japan’s largest business lobby, Keidanren, has even invited activist hedge funds to governance discussions, signifying a shift in institutional attitudes toward engagement.

This context matters: activism in Japan today is not episodic — it is systemic. It creates strategic impetus for boards to evaluate alternatives to status-quo capital structures, including take-privates and recapitalizations, especially where public valuations fail to reflect intrinsic business value.

II. The Growth of Esoteric ABS Technology in Japan: SMRAI Breaks Ground

While governance has driven strategic urgency, Japan’s capital markets have concurrently evolved in technical sophistication. Historically, the country’s asset-backed securities (ABS) market focused on traditional collateral such as mortgages and auto loans. But 2025 marked a notable inflection: Hilton Grand Vacations Japan Trust 2025-1 (“SMRAI”), a securitization of Japanese timeshare loans, successfully issued ¥9.5188 billion of AAA-rated notes — a landmark in structured finance for brand-linked consumer receivables in Japan.

According to press reports, SMRAI’s AAA-rated notes at a 1.41% coupon were placed efficiently with investors, highlighting both continued investor demand and the willingness of rating agencies and structurers to innovate beyond conventional collateral types.

This development is not a franchise royalty securitization per se, but it signalizes the increased technical capacity of Japanese markets to structure, rate, and absorb securitized exposures tied to diversified recurring consumer revenue streams. It demonstrates that esoteric ABS instruments can be executed effectively in Japan, and provides a template for future transactions backed by similarly predictable cash flows.

III. Underutilized ABS Markets and Macro Growth Potential

The broader context for securitization innovation extends beyond Japan. In Europe, where securitization markets lag significantly behind those in the United States, economists like Torsten Slok of Apollo Global Management have argued that improving securitization infrastructure could support meaningful GDP growth by lowering funding costs, broadening credit channels, and catalyzing investment. While Slok’s work focuses on European market structures, its macroeconomic logic — that deeper securitization markets can improve capital efficiency and support economic activity — is directly relevant to countries with underdeveloped structured finance ecosystems such as Japan.

Viewed through this lens, Japan’s evolving ABS market, exemplified by SMRAI and similar transactions, represents not just technical innovation but potential macroeconomic leverage: mobilizing institutional capital toward diversified assets that historically remained bank-held or on corporate balance sheets.

This, coupled with a weaker Yen significantly lowers the entry cost from foreign buyers, another growing point of contention as Japan deals with rising inflation, increased foreign ownership and commitments to be an open financial market.

IV. The Subway Securitization Blueprint: M&A Meets Structured Finance

A practical demonstration of securitization’s role in large LBOs emerged prominently in the U.S. with Subway’s securitization-linked financing. Following its acquisition by Roark Capital Group in 2024, Subway executed a $3.35 billion asset-backed bond sale, leveraging franchise fee revenues and related assets to fund the buyout — one of the largest whole-business securitizations on record.

This transaction broke new ground in M&A financing: by pledging franchise royalties and other contractual cash flows into a securitized vehicle, the deal delivered substantial liquidity that could service acquisition debt and refinance more expensive bridge facilities. The breadth and demand for the bonds — driven by orders far exceeding available paper — illustrated investor appetite for structured cash flows with predictable characteristics.

Subway’s securitization is noteworthy not just for its size but for its functional role: it demonstrates how recurring, diversified revenue streams tied to franchise networks can be transmuted into high-quality collateral capable of facilitating premium take-private pricing without disproportionate corporate leverage.

V. Convergence: From Governance Surplus to Financing Modernization

What unifies the narratives of rising activism, ABS innovation, macro underutilization, and structured M&A finance is the emergence of a convergence zone wherein Japanese corporate restructuring — especially in franchise-heavy industries — becomes both strategically imperative and financially executable.

Activism creates the strategic imperative to explore alternatives to the public status quo: Japan’s boards face pressure to improve capital allocation, enhance shareholder returns, and consider privatization or structural repositioning when markets systematically undervalue fundamental assets. SMRAI and related ABS innovation demonstrate that financial markets are increasingly capable of absorbing credit structures tied to predictable, contractually defined cash flows. Macroeconomic discussions like Apollo’s mobilize the conceptual case that securitization is not just credit engineering but a growth-enhancing market mechanism.

Subway’s securitization serves as the practical template.

Together, these dynamics suggest that franchise-royalty securitization could become a viable financing foundation for leveraged buyouts of Japanese franchise food operators — companies where:

- systemwide brand strength and unit-level revenue predictability yield predictable royalty streams,

- financial engineering reduces reliance on traditional corporate leverage, and

- activist pressure aligns board incentives toward strategic alternatives.

VI. Public Japanese Franchise Food Operators: Structural Candidates

Publicly traded Japanese food franchise operators often combine broad unit footprints, enduring brand equity, and recurring contractual cash flows in the form of royalty and service fees. Under rising governance pressure and given the evolution of Japan’s ABS market, such companies may become attractive candidates for take-private transactions or accelerated share repurchases financed or supported in part by securitized royalty streams.

Accelerated Share Repurchases (ASRs) are also growing in Japan — often structured as fully committed share repurchase (FCSR) transactions. They were developed to allow listed companies to execute large, rapid buybacks in a manner broadly similar to U.S.-style ASRs, but tailored to Japan’s legal framework. The structure typically involves an initial bulk purchase of shares through the Tokyo Stock Exchange’s ToSTNeT-3 off-auction system, followed by a later adjustment mechanism tied to the volume-weighted average price over a specified period. This approach enables companies to lock in a substantial repurchase upfront while economically aligning the final outcome with prevailing market prices.

Legally, ASRs must navigate strict requirements under Japan’s Companies Act, particularly rules governing shareholder equality, distributable amounts, and pricing fairness. The total cash consideration must be fixed at the outset to ensure compliance with statutory limits on distributable profits, and the structure must avoid conferring “specially favorable” terms that would require additional shareholder approval. Detailed disclosure is also critical to address insider trading and market transparency rules. As a result, Japanese ASRs reflect a careful adaptation of U.S. buyback mechanics within a more procedurally constrained corporate law regime.

Examples could include companies with large franchise systems trading at valuation discounts relative to global peers and exhibiting conservative balance sheet structures. In a world where activist voices are pushing for improved returns and boards must justify strategic alternatives, securitization offers sponsors a differentiated financing path — one that bridges predictable revenue and long-term strategic capital.

VII. Case Study: Mos Food Services Inc. (#8153)

Mos Food Services, Inc. is a publicly traded Japanese restaurant company best known for its MOS BURGER chain, one of Japan’s largest domestic fast-food brands. The company operates a predominantly franchise-based model, with the majority of its ~1,300+ Japan locations run by franchisees, complemented by a smaller number of company-owned stores. International expansion is concentrated in Asia (including Taiwan, Hong Kong, Singapore, Thailand, and Korea) and is typically executed through master franchise or joint venture partnerships. Overall, Mos Food Services has significant franchise exposure, with franchised and partner-operated stores representing the core of its unit footprint and growth strategy.

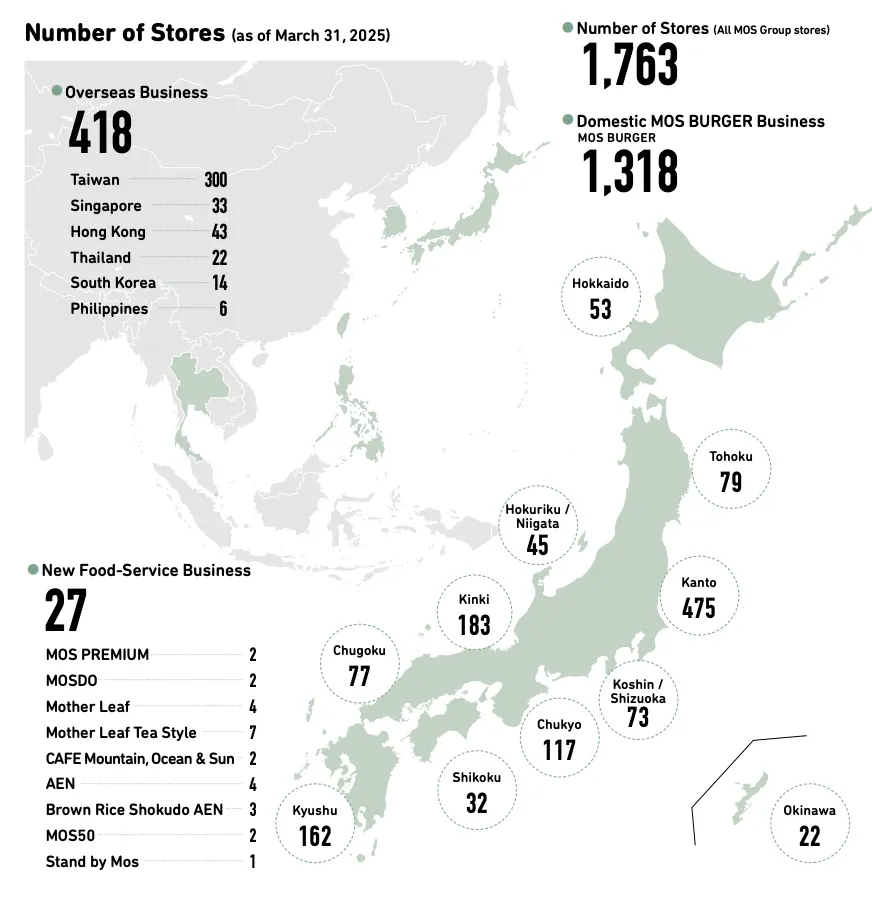

Let's dig into their financial statements. First, the integrated report shows several properties sprinkled across Japan and Internationally.

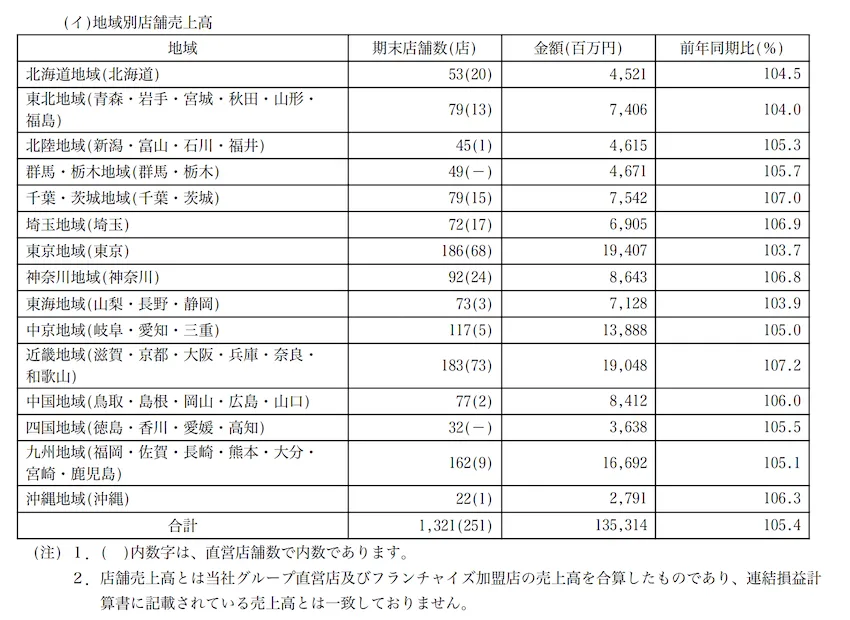

Based on their Annual Securities Report, of these 1321 locations, only 251 are company owned, meaning nearly 1,000 are franchised out in a model similar to the United States.

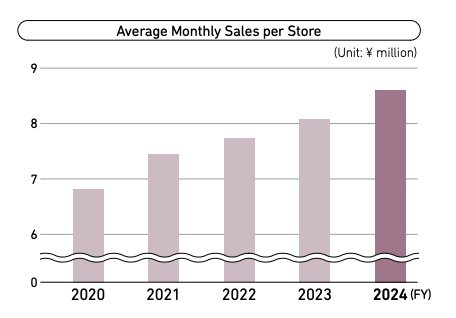

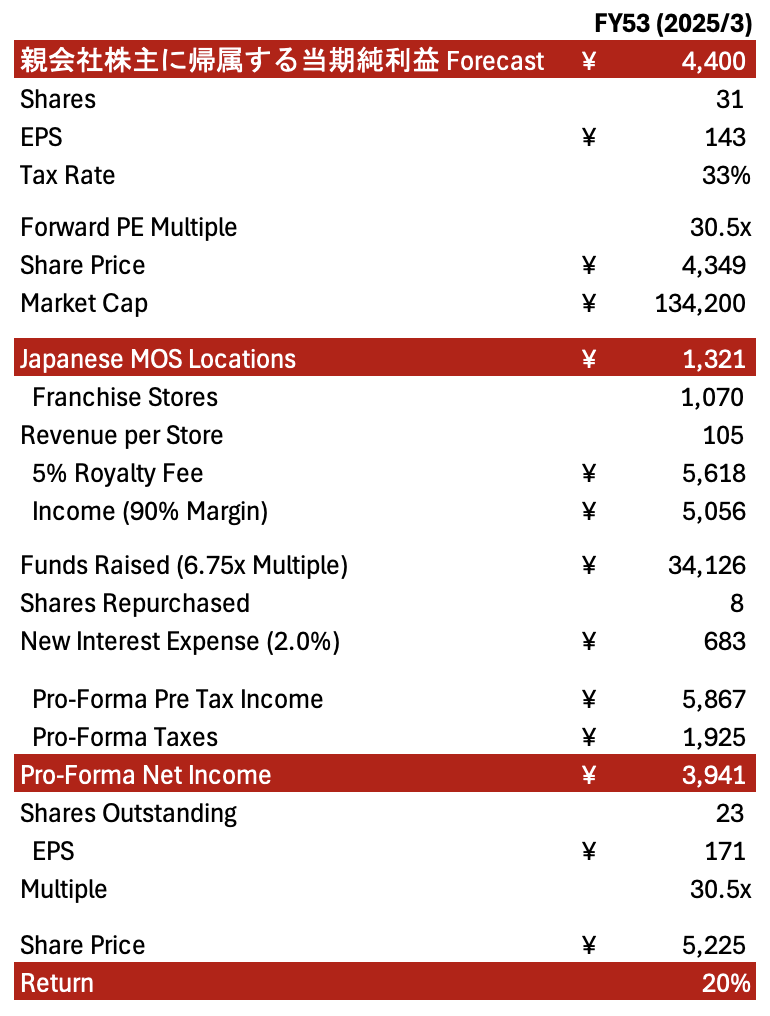

MOS reports its results and forecast here, so for smoothed 親会社株主に帰属する当期純利益, we'll assume about ¥4,400 for a full year and 31M shares outstanding. MOS stores have average monthly sales of about ¥8 - ¥9M.

Assuming the 1,000 stores are doing something in this range with a little growth for future year and the royalty fee is 5%, that's ~¥5,600 in revenues, and assuming a 90% margin on franchise fees (US ranges 85-90%), that's just over ¥5,000 in EBITDA for that business. While whole business or contractual cash flow multiples range from 4-6.5x, it's not inconceivable to think these could run closer to 6.75x given the exceptionally low default ratios in Japan relative to other Western markets.

Pulling that together, assuming a 2% cost of debt for this type of transaction based on current benchmarks, the incremental interest expense is only ¥708 with over ¥35,000 raised. Redeploying that to an ASR lowers the share count materially, meaning even at the lower 親会社株主に帰属する当期純利益 the lower share count creates an immediate 20% return.

Additionally, typically valuation on an EV/EBITDA basis excludes non-recourse SPV/SPC debt so it immediately becomes accretive to share price and valuation.

These are the type of debt financing transactions that could either support acquisition buyouts or accelerate short-term gains by monetizing stable cash flows and lowering share count through share repurchases, which in Japan are estimated to reach all-time highs. Share repurchase authorizations from April through December 2025 reached ¥14.2 trillion, based on estimates compiled from the Tokyo Stock Price Index (TOPIX). The largest program was unveiled in April by Mitsubishi Corporation, with a ceiling of ¥1 trillion.

VIII. Macro Implications: From Transactional Innovation to Structural Growth

If franchise royalty securitization were to gain traction as a standard tool in Japan, the implications would extend beyond isolated buyouts or share buybacks. A deep and liquid structured finance market could:

- broaden the universe of collateral types for institutional investors,

- improve funding efficiency for predictable corporate cash flows,

- facilitate capital recycling within Japanese equity and credit markets, and

- strengthen Japan’s integration with global structured finance norms.

The combination of governance change and capital markets innovation — evidenced in activism trends and ABS transactions like SMRAI — suggests Japan could be on the cusp of a structural bonanza: one in which monetizable, predictable cash flows across franchise systems enable a new wave of leveraged corporate restructurings, supported by sophisticated securitization engineering.

{kind=link}