Table of Contents

The past week offered a rare moment of clarity in credit markets—not because volatility subsided, but because a single theme began to connect what otherwise appear to be disparate developments. That theme is infrastructure, and more specifically, the quiet but accelerating transformation of data centres into one of the defining asset classes of modern credit markets.

At the centre of that shift sits the APLMA’s new white paper, “Network Effects: How Data Centre Financing is Reshaping Loan Markets in Asia Pacific” . While framed as a sector study, it reads more like a structural blueprint for how capital is reorganizing itself around the digital economy.

Data Centres as the New Core Infrastructure

For years, data centres were described—often lazily—as a form of “digital real estate.” The APLMA paper makes clear that this framing has outlived its usefulness. What is emerging instead is something far more complex: an asset class that blends infrastructure stability with technology-driven volatility.

The distinction matters. Traditional real estate underwriting relies on relatively stable assumptions—location, tenant diversification, lease duration, and physical depreciation. Data centres, by contrast, derive their economic value from forces that sit outside the building itself. Power availability, network connectivity, customer concentration, and even chip architecture increasingly dictate performance. The building is necessary, but it is no longer sufficient.

This reclassification is already reshaping how lenders approach the asset. A facility leased to a hyperscale tenant on a long-term contract behaves very differently from a multi-tenant colocation site with shorter-duration agreements. In the former, credit risk is effectively a function of the tenant—often one of a handful of global technology firms. In the latter, the risk shifts toward operational execution, churn management, and the ability to continually upgrade infrastructure in line with customer needs.

What becomes clear is that data centres do not sit neatly within any existing asset class. They are not purely infrastructure, not purely real estate, and not purely corporate credit. They are all three at once, and that hybridity is precisely what is attracting—and challenging—capital.

Demand Is Not the Question—Its Shape Is

If the supply of capital is adjusting, it is doing so in response to demand that is both extraordinary in scale and evolving in character. Asia Pacific alone already hosts roughly 1,800 data centres, with total capacity expected to approach 24 gigawatts by the end of the decade . But the more important story lies beneath those headline numbers.

Artificial intelligence is no longer simply an incremental driver of data usage; it is redefining the physics of demand. AI workloads require dramatically higher power density, more sophisticated cooling, and closer integration between hardware and infrastructure. At the same time, the rise of edge computing is pushing smaller facilities closer to end users, fragmenting what was once a more centralized model.

This combination—centralized hyperscale growth alongside decentralized edge expansion—creates a market that is both scaling rapidly and becoming more complex. For lenders, this means that visibility into demand is unusually strong, but predictability at the asset level is less certain than it might appear.

Capital at Scale, and the Reordering of Credit Markets

It is when the discussion turns to financing that the paper becomes most revealing. Data centres are extraordinarily capital intensive, requiring large upfront investment and continuous reinvestment to remain technologically relevant. This is not a one-time financing problem; it is an ongoing capital commitment.

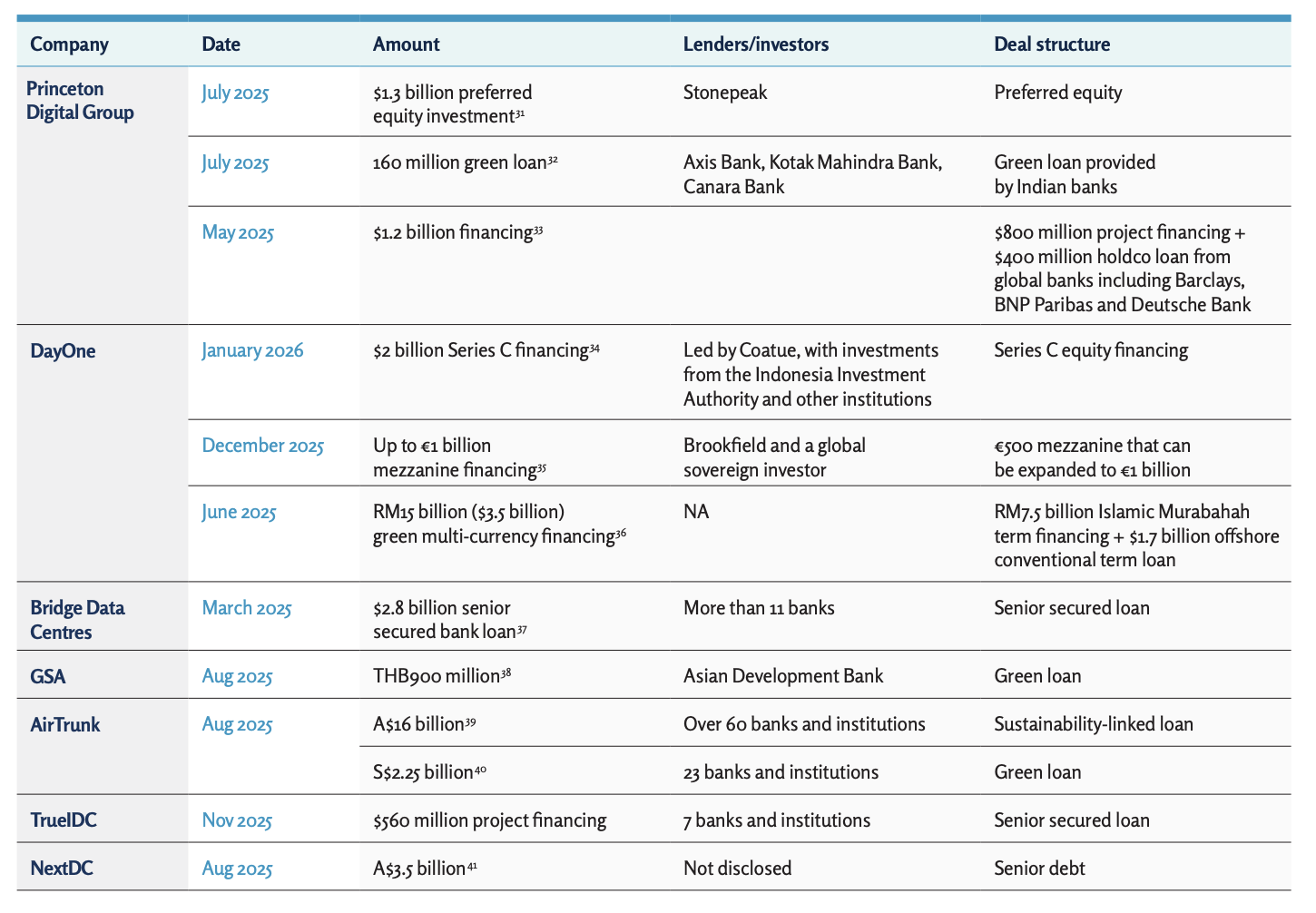

As a result, the structure of financing itself is evolving. Banks are no longer the sole providers of debt capital. Instead, they are increasingly working alongside private credit funds, infrastructure investors, and institutional capital pools. This is not merely a matter of diversification—it reflects the limits of traditional balance sheets in absorbing the scale and complexity of these assets.

At the same time, capital structures are becoming more layered. Senior secured debt is often complemented by mezzanine financing, holdco-level capital, and, in some cases, structured or quasi-equity instruments. These layers introduce additional complexity, particularly around intercreditor dynamics and enforcement rights, areas that the paper highlights as requiring careful legal structuring.

What emerges is a financing ecosystem that looks less like traditional project finance and more like a hybrid between infrastructure funding and leveraged finance. It is an ecosystem still in the process of defining its own norms.

Geography, Power, and the Limits of Growth

One of the more subtle but important insights in the paper is the role of geography—not as a proxy for demand, but as a constraint on supply. Historically, data centre development clustered in major hubs such as Tokyo, Singapore, and Hong Kong. Increasingly, however, developers are being pushed outward.

The reason is not demand saturation, but resource scarcity. Power availability, land constraints, and regulatory limitations are forcing development into secondary markets such as Osaka, Johor, and Melbourne. In this sense, the most important input into data centre financing is not capital, but electricity.

This introduces a new dimension to credit analysis. Access to reliable, scalable energy becomes as critical as tenant quality. In some cases, it may be more critical.

The Uncomfortable Truth: Obsolescence and Regulation

For all the optimism surrounding the sector, the risks are neither trivial nor easily dismissed. Perhaps the most fundamental is the risk of technological obsolescence. Unlike traditional infrastructure, which can operate effectively for decades, data centres face rapid cycles of technological change. Cooling systems, power density, and hardware requirements evolve quickly, shortening the economic life of assets and complicating long-term financing assumptions.

Layered on top of this is regulatory complexity. Data sovereignty rules, cross-border restrictions, and local compliance requirements vary significantly across Asia Pacific. These are not static risks; they evolve alongside geopolitical dynamics, adding an additional layer of uncertainty to what is already a complex asset class.

And yet, despite these risks, capital continues to flow. In part, this reflects the absence of viable alternatives offering comparable scale and growth. In part, it reflects a broader shift in how investors think about infrastructure itself.

Macro Undercurrents: Fragility Beneath Stability

Set against this structural transformation, the week’s broader credit developments provide a useful counterpoint. On the surface, markets appear stable. Ratings remain largely intact, and systemic stress is contained. But beneath that stability, early signs of pressure are becoming visible.

The most striking example comes from geopolitics. The prolonged Iran conflict is now introducing a highly specific but potentially consequential risk to semiconductor supply chains, through disruptions to helium supply. Helium is a critical input in chip manufacturing, and shortages could ripple through production, increasing costs and forcing prioritization of output .

This is a reminder that even the most advanced segments of the digital economy remain tethered to physical supply chains—chains that are vulnerable to geopolitical disruption.

China: A Market of Diverging Signals

In China, the picture is similarly nuanced. Regulatory efforts have made parts of the financial system more transparent, reducing risks associated with opaque lending structures. At the same time, underlying asset performance is beginning to weaken.

The deterioration in auto ABS collateral is particularly notable. Default rates have risen sharply, with annualized gross losses increasing to 1.13% in the fourth quarter of 2025, up from 0.75% in the prior quarter . While some of the earlier weakness was obscured by technical factors, the latest data suggests that underlying credit conditions are softening.

Residential mortgage-backed securities, by contrast, remain more stable, though they too are showing early signs of pressure. The divergence between asset classes underscores a broader theme: credit structures may remain resilient, but collateral performance is beginning to tell a different story.

Policy responses are attempting to bridge this gap. Measures to support consumer credit, including interest subsidies and credit repair initiatives, are designed to stabilize demand and expand access to financing. Yet these interventions also risk distorting traditional credit signals, making it more difficult to assess borrower quality using historical metrics.

ABS Asia: A Timely Convergence

All of these themes—structural transformation in infrastructure, emerging macro risks, and evolving credit performance—converge as ABS Asia begins tomorrow.

The conference arrives at a moment when markets are neither in crisis nor at ease. Instead, they are in transition. Data centres and digital infrastructure are redefining where and how capital is deployed. At the same time, asset-level performance is beginning to soften, even as structural protections hold.

This tension—between resilience and deterioration, between innovation and risk—will likely define the discussions in the days ahead.

Closing Reflection

If there is a single takeaway from the week, it is that credit markets are being reshaped from the ground up—quite literally. The infrastructure that underpins the digital economy is becoming the infrastructure that underpins the credit system itself.

Data centres are not just absorbing capital; they are reorganizing it. They are forcing lenders to rethink underwriting, investors to rethink allocation, and markets to rethink what constitutes a stable, long-duration asset.

As ABS Asia begins, that shift is no longer theoretical. It is already underway.

{kind=link}