Table of Contents

Policy momentum, structural innovation, and the road to ABS Asia

As the Asian structured-finance community prepares to gather for ABS Asia next week, the region’s securitization markets are entering what may prove to be their most dynamic phase in more than a decade. Across China, Japan, and other regional markets, issuance is expanding, new asset classes are emerging, and policymakers are increasingly turning to securitization as a mechanism to support broader economic objectives.

In many respects, the story of securitization in Asia today is no longer simply about funding. Instead, it is becoming a platform through which regulators and financial institutions are experimenting with new models of capital formation—ranging from consumer credit and infrastructure to intellectual property and green finance.

The result is a market that is steadily expanding in scale while simultaneously evolving in structure.

Macro backdrop: rising rates and the return of duration

The macro environment surrounding Asia’s fixed-income markets is also beginning to shift in important ways. In Japan, for example, investors are closely watching this week’s 20-year Japanese government bond auction, which some market participants believe could prove just as important for the near-term narrative as the Bank of Japan’s policy meeting.

The auction will provide an early signal of how concerned investors have become about the country’s inflation outlook following the recent surge in oil prices. Traders may use the debt sale to gauge the market’s tolerance for higher yields, potentially shaping expectations ahead of any future shift toward tighter monetary policy.

The long end of Japan’s yield curve has historically been volatile, and 20-year auctions in particular are often characterized by uneven demand. Analysts suggest that a bid-to-cover ratio below 3.0 would reinforce the theme of yield-curve steepening, as investors demand greater compensation to hold longer-duration debt.

For securitization markets, these dynamics matter. Structured credit products—particularly highly rated ABS and RMBS tranches—often compete directly with government bonds for allocation from insurers, pensions, and bank treasuries. As yields in government bond markets rise, the relative value of structured products becomes increasingly important.

A market quietly gaining momentum

Against this macro backdrop, issuance across Asia’s securitization markets continues to expand. Some of the clearest evidence comes from China, which now represents one of the largest securitization ecosystems outside the United States.

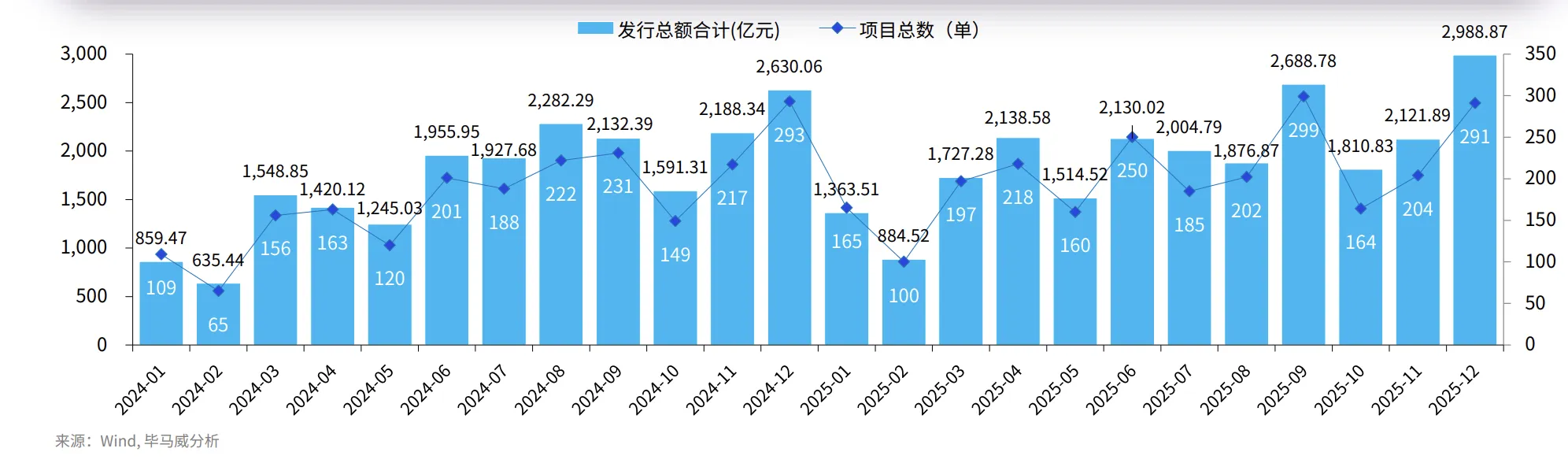

According to KPMG’s most recent review of the Chinese market, the country’s asset securitization sector continued to grow steadily in 2025, with 2,435 new transactions issued during the year and total issuance reaching RMB 2.33 trillion.

The expansion was broad-based. Corporate ABS remained the largest segment of the market, accounting for more than RMB 1.4 trillion in issuance, while asset-backed notes and credit ABS continued to gain traction. Public REITs also contributed to overall issuance volumes as regulators broadened the scope of securitization structures available to investors.

Beneath these aggregate numbers lies a market increasingly defined by the diversity of its underlying assets. Financing lease receivables, consumer loans, and corporate receivables have emerged as the dominant collateral types, forming what industry analysts often describe as the “three pillars” of China’s ABS market. Together these asset classes accounted for roughly 42% of total securitization volume in 2025.

Yet the deeper story may be the direction of regulatory policy shaping this growth.

Securitization as a policy tool

Unlike the more market-driven evolution of securitization in the United States and Europe, Asia’s structured-finance markets often develop alongside explicit policy objectives. In China particularly, securitization has increasingly been used as a mechanism to channel capital into priority sectors of the economy.

Recent regulatory developments illustrate how this dynamic is unfolding. Authorities have expanded the framework for public REITs beyond traditional infrastructure assets to include commercial real estate, opening the door to a wider range of income-producing properties entering capital markets structures.

At the same time, policymakers have emphasized the role of securitization in supporting consumer lending. Guidance released by multiple government agencies in 2025 encouraged the expansion of securitization for retail credit assets such as automobile loans, credit-card receivables, and consumer finance loans.

Other initiatives suggest even more experimentation may lie ahead. Regulators have encouraged financial institutions to explore securitization backed by intellectual property rights, while green finance initiatives are promoting the development of environmentally linked ABS products.

Taken together, these initiatives point toward a broader transformation in how securitization is being used—less as a purely financial engineering tool and more as a mechanism for supporting economic policy goals.

A mature benchmark market in Japan

While China’s securitization market has been characterized by rapid expansion and experimentation, Japan remains one of the most stable and institutionalized structured-finance markets in Asia.

A recent example illustrates this stability. S&P Global Ratings recently assigned a preliminary AAA (sf) rating to the 227th issuance of mortgage-backed securities from the Japan Housing Finance Agency (JHF), part of the long-running Flat 35 mortgage program.

The transaction securitizes pools of fixed-rate residential mortgages originated by Japanese lenders and distributed through the government-supported housing finance system. Mortgage payments from borrowers are passed through to investors, creating predictable cash flows backed by standardized underwriting and servicing frameworks.

Over time, the Flat 35 program has evolved into one of the most important securitization platforms in Asia. For domestic investors—particularly insurers and pension funds—it provides a consistent supply of highly rated structured bonds that function as a benchmark product within the region’s credit markets.

In many ways, the program serves as Japan’s closest analogue to the U.S. agency mortgage market.

A market entering its next chapter

Looking across Asia today, several themes appear to be converging.

Securitization markets are expanding steadily in scale. The growth of issuance volumes in China, combined with the stability of mature programs such as Japan’s RMBS market, suggests that securitized credit is becoming an increasingly integral part of the region’s financial system.

At the same time, the range of securitized assets continues to broaden. Traditional collateral types such as mortgages, auto loans, and receivables remain dominant, but newer structures backed by real estate income streams, intellectual property rights, and environmental projects are beginning to appear.

Finally, regulatory policy continues to shape the direction of these markets. Governments across Asia increasingly view securitization not merely as a funding tool but as a way to support broader economic priorities—from consumer spending to infrastructure development.

Looking ahead to ABS Asia

These themes are likely to dominate discussions at ABS Asia next week, where investors, arrangers, and policymakers will gather to assess the future trajectory of the region’s structured-finance markets.

The questions facing the industry are becoming more complex. Will Asia’s securitization markets deepen enough to attract sustained global investor participation? Which emerging asset classes will prove scalable? And how will rising interest rates reshape the relative value of structured credit compared with sovereign debt?

What seems increasingly clear, however, is that securitization in Asia is entering a new phase—one defined not just by growth, but by innovation and policy integration.

As ABS Asia convenes, the region’s structured-finance market may be approaching a pivotal moment.

{kind=link}