Table of Contents

Japanese officials moved quickly this week to calm markets after a sharp selloff in government bonds sent ultra-long yields to levels not seen in decades. The volatility followed a surprise campaign pledge by Sanae Takaichi to temporarily cut taxes on food and non-alcoholic beverages—an announcement that revived investor concerns over fiscal discipline in a country already carrying one of the world’s heaviest public-debt burdens.

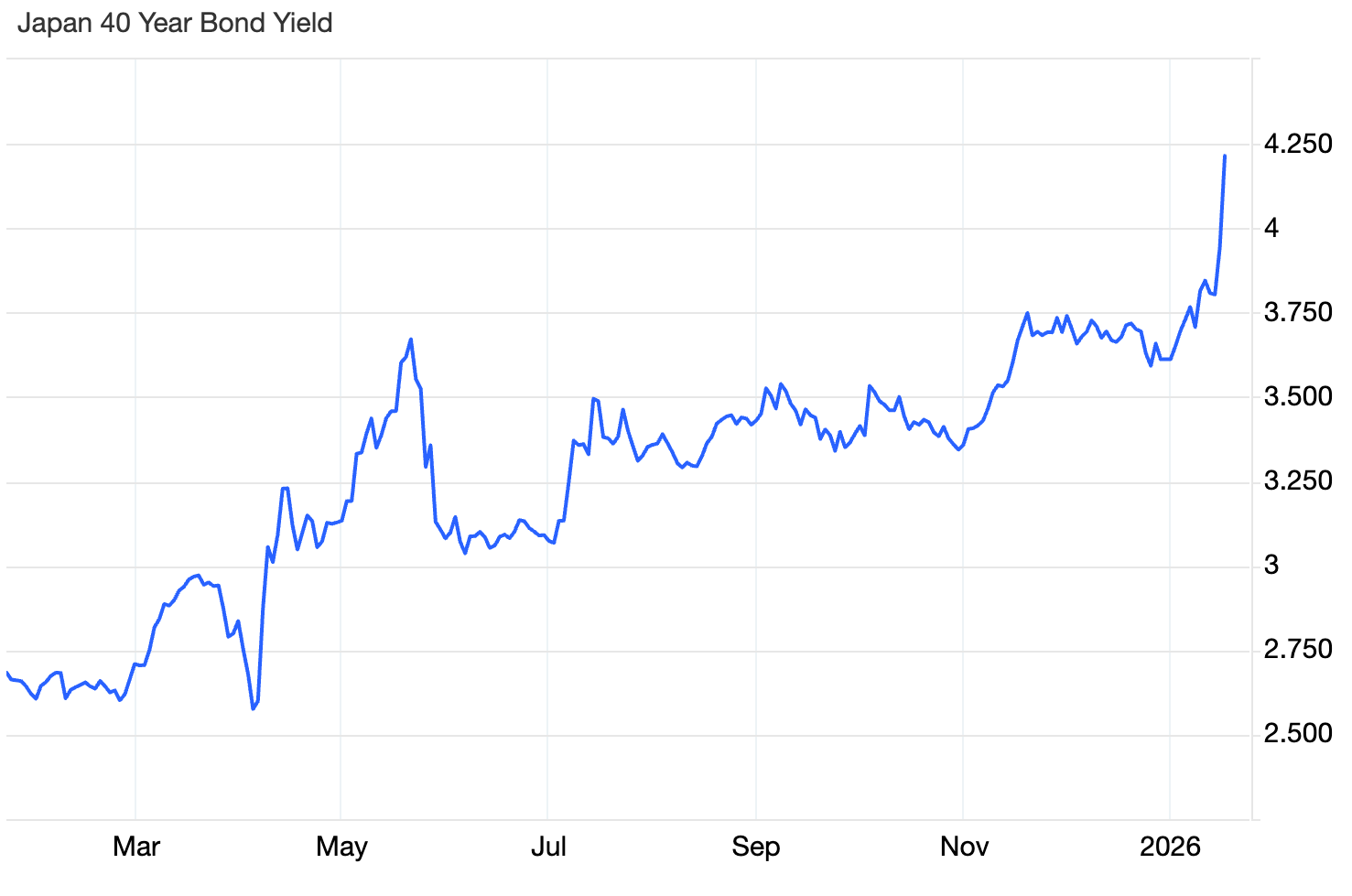

On Tuesday, long-term Japanese government bond (JGB) yields spiked, with the 40-year yield briefly surging past 4%—a record since the maturity’s introduction in 2007 and the highest for any Japanese sovereign tenor in more than three decades. The move prompted questions about whether markets are beginning to demand a higher risk premium for Japan’s fiscal trajectory.

Government spokesperson Minoru Kihara sought to downplay the turmoil, emphasizing that long-term yields are shaped by many factors and determined by the market. He reiterated the government’s commitment to sustainable fiscal policy and to reducing the debt-to-GDP ratio, while noting that officials are monitoring market developments closely.

That reassuring message was echoed abroad. Speaking on the sidelines of the World Economic Forum in Davos, Finance Minister Satsuki Katayama said Japan would maintain fiscal sustainability even as it seeks to support growth. Trade Minister Ryosei Akazawa, for his part, struck an optimistic tone, arguing that now was a good time to buy Japanese assets.

A Tax Cut Without a Funding Plan

The catalyst for the market reaction was Takaichi’s pledge to suspend an 8% sales tax on food and non-alcoholic drinks for two years. While popular with voters grappling with rising living costs, the proposal comes with a hefty price tag—around ¥5 trillion ($31.6 billion) per year, according to the Finance Ministry. That sum is roughly equivalent to Japan’s combined annual spending on education, science, and culture.

Crucially, the prime minister has yet to explain how the shortfall would be financed. Until there is clarity on whether the government can cover the gap without issuing additional deficit-financing bonds, investors appear wary. The episode has drawn comparisons to the UK’s 2022 market turmoil under former Prime Minister Liz Truss—though Japan’s proposed tax cut is far smaller in relative terms.

Pressure on the BOJ

The selloff comes at an awkward moment for the Bank of Japan, which has been carefully stepping back from its long-standing role as a dominant buyer of government bonds since March 2024. With the BOJ’s policy meeting scheduled for later this week, most economists expect rates to be left unchanged following last month’s hike. Still, another sharp rise in yields could force the central bank to consider ramping up bond purchases—an outcome policymakers would prefer to avoid.

BOJ officials have previously made clear that they stand ready to intervene if market volatility becomes excessive, but the broader shift away from heavy bond buying is itself contributing to nervousness. Investors, long accustomed to the central bank’s stabilizing presence, are now testing how much volatility the market can absorb.

Politics Meets the Bond Market

Takaichi’s tax pledge is widely seen as an election gambit ahead of a Feb. 8 lower-house vote, with inflation a top concern among voters. Yet the strategy underscores a delicate balancing act: delivering relief to households while convincing investors that fiscal policy will not spiral out of control.

Opposition parties have complicated the picture further by proposing even more aggressive tax cuts, some of which would cost significantly more than Takaichi’s plan. While Japan’s recent inflation has boosted nominal growth and helped lower the debt-to-GDP ratio, analysts caution that rising interest rates could quickly offset those gains by increasing debt-servicing costs.

As one strategist put it, markets are becoming more sensitive to signs of fiscal expansion and are demanding higher compensation for long-term risk. For now, officials insist there is no cause for panic. But until funding details emerge, Japan’s bond market is likely to remain on edge—watching closely to see whether campaign promises translate into a lasting shift in fiscal policy.

Anticipated Impact on Structured Finance Markets

Rising volatility at the long end of Japan’s government bond curve is already spilling into the structured finance market. As ultra-long JGB yields reprice on fiscal uncertainty, ABS investors are demanding wider spreads, particularly on longer-dated and subordinated tranches. While underlying collateral performance across Japanese auto, consumer, and esoteric ABS remains stable, higher risk-free rates and term premiums are pushing up all-in funding costs and compressing execution flexibility for issuers.

For now, the impact is more about pricing than pipeline disruption. Sponsors with strong structures, shorter weighted-average lives, or access to offshore demand are likely to remain active, while marginal or more duration-heavy deals may be delayed. If fiscal clarity improves and volatility subsides, ABS issuance should normalize. But a prolonged period of JGB instability would mark a clear shift: Japan’s ABS market moving from a central-bank-anchored environment to one where macro policy risk plays a much larger role in deal execution and investor behavior.

{kind=link}